Other key indicators include the January Personal Income and Outlays report on Monday, February ISM manufacturing index also on Monday, February vehicle sales on Tuesday, the ISM non-manufacturing index on Wednesday, and the January Trade Deficit on Friday.

8:30 AM ET: Personal Income and Outlays for January. The consensus is for a 0.4% increase in personal income, and for a 0.1% decrease in personal spending. And for the Core PCE price index to increase 0.1%.

10:00 AM: ISM Manufacturing Index for February. The consensus is for a decrease to 53.0 from 53.5 in January.

10:00 AM: ISM Manufacturing Index for February. The consensus is for a decrease to 53.0 from 53.5 in January.Here is a long term graph of the ISM manufacturing index.

The ISM manufacturing index indicated expansion in January at 53.5%. The employment index was at 54.1%, and the new orders index was at 52.9%

10:00 AM: Construction Spending for January. The consensus is for a 0.3% increase in construction spending.

All day: Light vehicle sales for February. The consensus is for light vehicle sales to increase to 16.7 million SAAR in February from 16.6 million in January (Seasonally Adjusted Annual Rate).

All day: Light vehicle sales for February. The consensus is for light vehicle sales to increase to 16.7 million SAAR in February from 16.6 million in January (Seasonally Adjusted Annual Rate).This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the January sales rate.

8:15 PM: Speech, Fed Chair Janet L. Yellen, Bank Regulation and Supervision, At the Citizens Budget Commission's Annual Awards Dinner, New York, New York

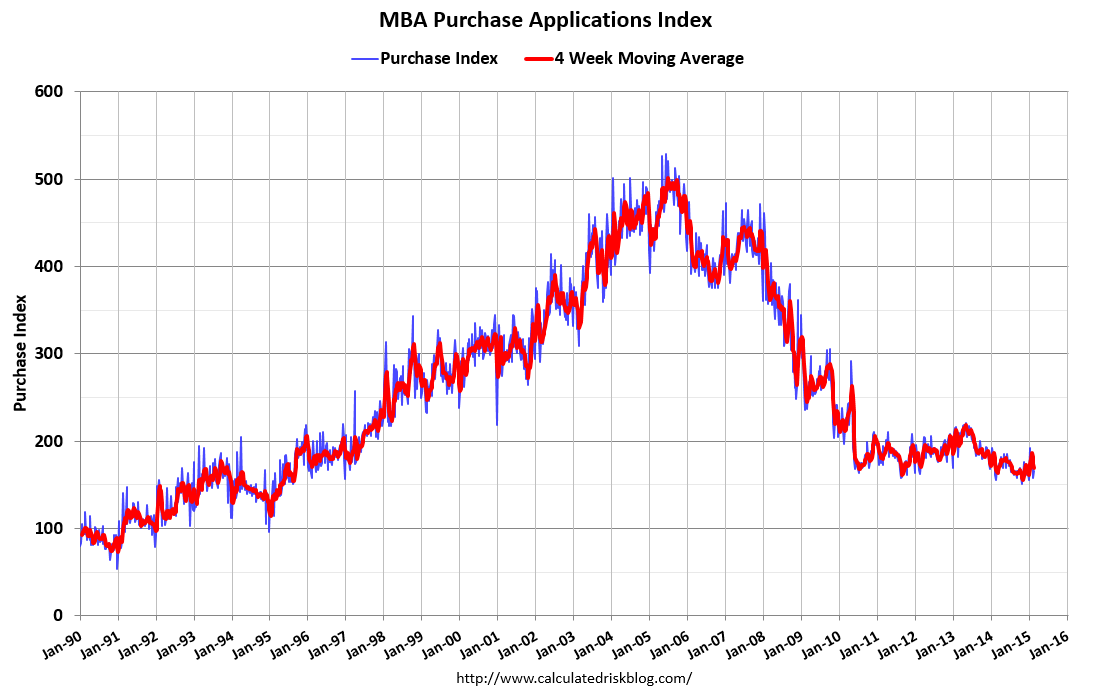

7:00 AM: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for February. This report is for private payrolls only (no government). The consensus is for 220,000 payroll jobs added in February, up from 213,000 in January.

10:00 AM: ISM non-Manufacturing Index for February. The consensus is for a reading of 56.5, down from 56.7 in January. Note: Above 50 indicates expansion.

2:00 PM: Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for claims to decrease to 300 thousand from 313 thousand.

10:00 AM: Manufacturers' Shipments, Inventories and Orders (Factory Orders) for January. The consensus is for no change in January orders.

4:30 PM: Dodd-Frank Act Stress Test Results

8:30 AM: Employment Report for February. The consensus is for an increase of 230,000 non-farm payroll jobs added in February, down from the 257,000 non-farm payroll jobs added in January.

The consensus is for the unemployment rate to decline to 5.6% in February from 5.7% in January.

This graph shows the year-over-year change in total non-farm employment since 1968.

This graph shows the year-over-year change in total non-farm employment since 1968.In January, the year-over-year change was 3.21 million jobs. This was the highest year-over-year gain since the '90s.

As always, a key will be the change in real wages - and as the unemployment rate falls, wage growth should start to pickup.

8:30 AM: Trade Balance report for January from the Census Bureau.

8:30 AM: Trade Balance report for January from the Census Bureau. This graph shows the U.S. trade deficit, with and without petroleum, through December. The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The consensus is for the U.S. trade deficit to be at $41.8 billion in January from $46.6 billion in December.

3:00 PM: Consumer Credit for January from the Federal Reserve. The consensus is for credit to increase $15.0 billion.